Grainger reported 1Q 2026 results on May 7, with sales of $4.7 billion, up 10.1%, or 12.2% on a daily, organic constant currency basis. They achieved an operating margin of 16.7%, up 110 basis points, reversing last quarter’s decline. Volume growth and higher customer demand drove Endless Assortment sales up 19.6%, and High Touch sales were up 10.5%. Grainger passed through tariff‑related cost increases, especially to its High Touch customers.

Grainger’s gross margin increased 30 bps to 40.0%. The UK exit – Cromwell divestiture + Zoro U.K. closure – and improved margins in both Business Segments contributed, with High‑Touch gross margin rising 20 bps.

(Food for thought … why can national chains seemingly improve overall gross margins with some type of regularity but independents don’t unless it is due to unexpected product mix, unexpected business mix, a focused pricing initiative, or, and rarely, major shifts in COGS (procurement)? Why isn’t this an ongoing mindset and initiative? Who should be a distributor’s “Profitability Czar” focused on seeking out ongoing profit improvement opportunities and then maintaining them?)

Grainger said tariffs created cost pressure, especially on private‑label inventory, and the company responded with selective price increases to maintain price‑cost neutrality. The CFO warned that higher‑cost tariff‑impacted inventory would shift margin pressure into Q2 2026. Price actions contributed about 5 percentage points of High‑Touch growth, including tariff pass-through actions (making organic growth only 5%.) Management emphasized that pricing would continue to be used to offset cost inflation, which includes tariff‑driven costs.

In the High-Touch Solutions – N.A. segment (HTS-NA) , typically “in-plant” and serving the Fortune 500 companies and most comparable to an industrial supply distributor’s standard customer, accounted for 75% of Grainger’s revenue in 2025.

Daily sales increased 10.5%, and 10.0% on a daily, constant currency basis to $3.75 billion. The strong sales drivers included healthy price contribution and volume growth. Gross profit margin increased 20 basis points, driven by positive mix and freight, which was partially offset by the impact of the annual Grainger Sales Meeting. Price and cost were roughly neutral.

This performance is comparable to the results from Industrial Supply Trends’ Pulse of Industrial Support Report.

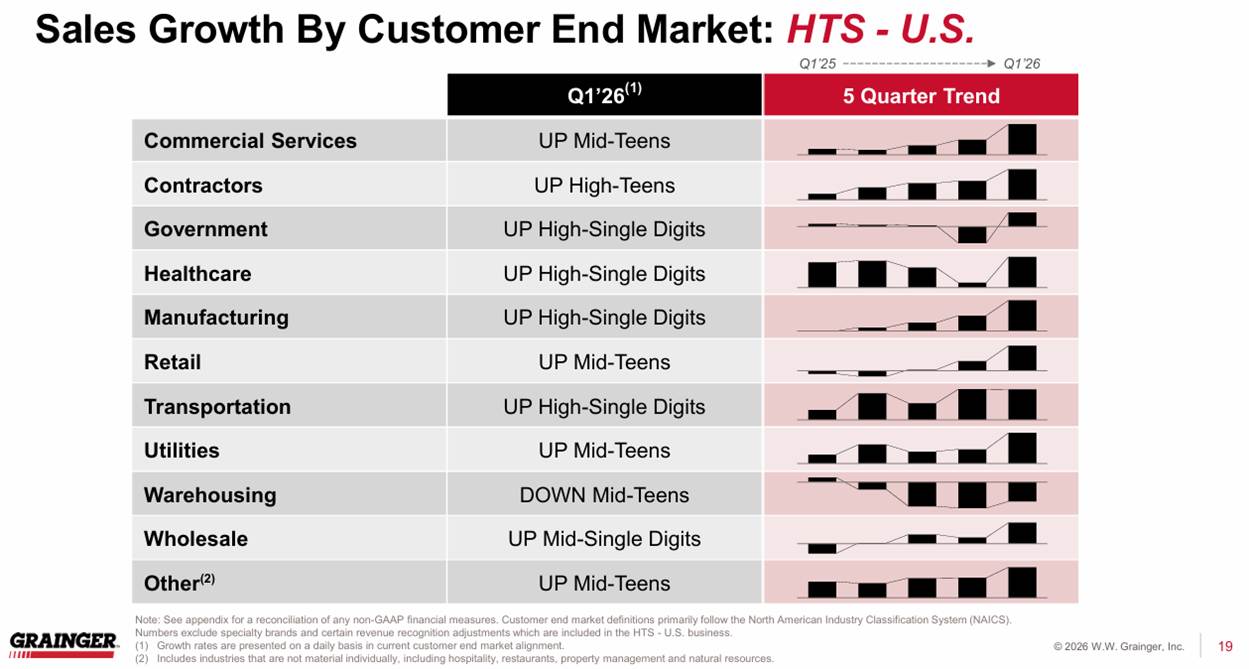

HTS‑N.A. growth was broad‑based, with manufacturing, government, and contractor customers called out explicitly as the strongest contributors. Manufacturing was the strongest contributor, as demand inflected positively as the MRO market turned volume‑positive. Growth was supported by Grainger’s on‑site service model and the ability to solve complex MRO needs. During the quarter federal, state, and local agencies increased MRO spending. Management highlighted strong traction with large contract customers, which includes government accounts. Contractor demand benefited from ongoing construction and infrastructure activity. Management highlighted Grainger’s high‑touch model (inventory availability + on‑site support) as a differentiator.

In HTS-N.A., midsized customers grew 14%, while large customers grew 9%. Grainger attributed this to uneven demand as mid‑size demand strengthened more materially, while large customers remained more cautious, particularly in certain verticals. Grainger’s investments in sales coverage, digital tools, and service enhancements reportedly are resonating with mid‑size customers, who typically have more fragmented procurement processes, making Grainger’s value proposition—availability, reliability, and service—more impactful (albeit something that independents can compete against cost-effectively.) HTS‑N.A. digital penetration remains extremely high, consistent at around 85%, driven by EDI, eProcurement integrations, KeepStock automated inventory systems and Grainger.com.

Sales growth in the quarter and the trend over the last 5 quarters is shown in the chart from the earnings presentation:

In the Endless Assortment segment (MonotaRO, Zoro), what could be called, “non-Grainger branded” for historically small and mid-sized customers who purchase periodically, sales were strong, up 19.6% reported and 21.9% on daily organic constant currency basis to $990 million. Growth was driven primarily by volume and price, with similar comments as HTS-NA. This segment is entirely on-line.

Zoro US sales were up 18.7% and MonotaRO sales increased 22.7% in local constant currency.

Analyst Questions

Analysts questioned whether Grainger could maintain its elevated gross margins. Management warned that higher‑cost private‑label inventory would shift from Q1 into Q2 and negatively impact margins next quarter. This created concern that Q1 margin performance was not fully repeatable and could pressure full year profitability.

Guidance

Grainger raised its full-year 2026 outlook to sales of $19.2 billion to $19.6 billion. Management emphasized continued momentum in HTS N.A. and noted that the strong Q1 performance and continued strong growth expectations for Endless Assortment, supported by digital adoption and customer acquisition trends contributing to raising full‑year 2026 guidance. The company said the increase reflects a strong start to the year and continued demand momentum despite tariff and geopolitical uncertainty.

Some Questions

- Given seasonality and expected Q2 hits to margin, is Q1 a high watermark? Is margin expansion repeatable?

- Is Endless Assortment growth of around 20% sustainable?

- Can Grainger’s pricing power and tariff pass throughs hold if tariffs change or if customers resist additional price increases?

- Rising fuel costs directly affect Grainger’s logistics‑heavy HTS business, raising concerns about operating margin compression in future quarters.

Leave a Reply