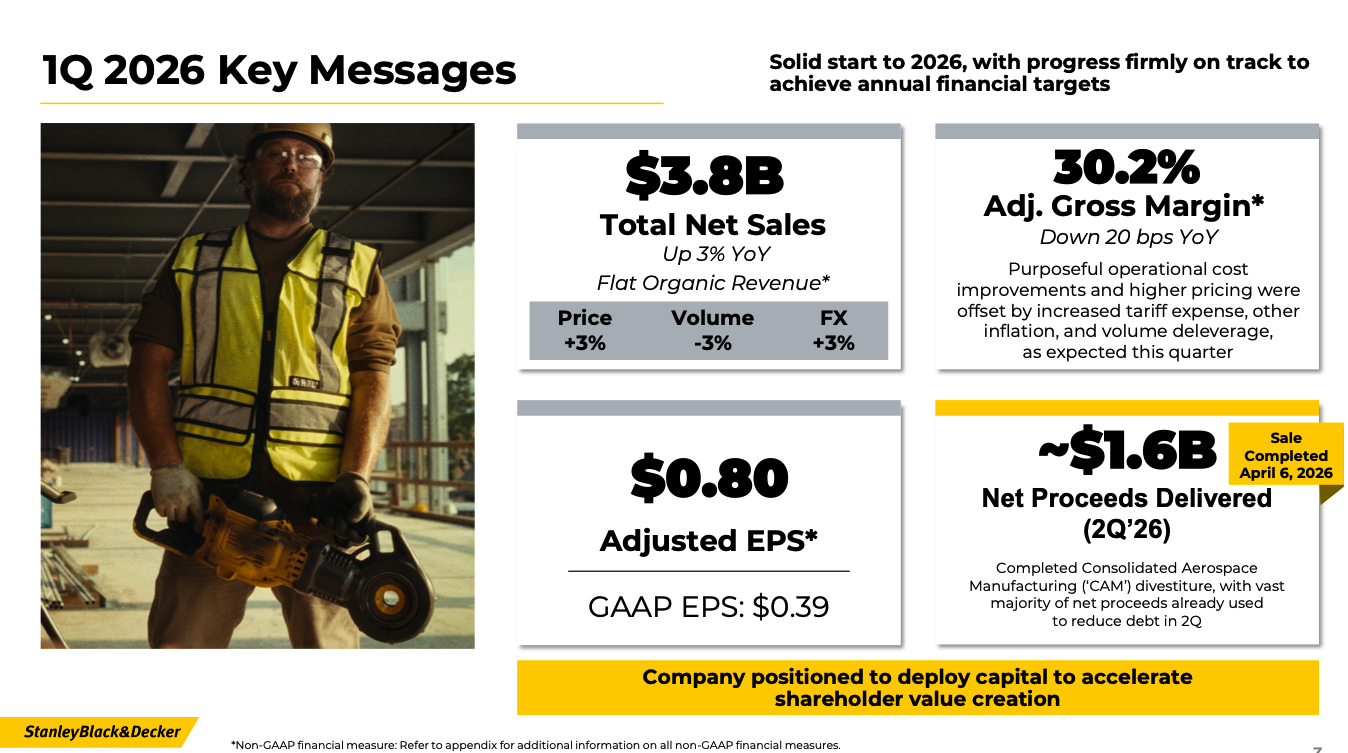

Stanley Black Decker Q1 2026 results landed this week. For the Stanley Black Decker industrial channel, the more useful read is what sits underneath the headline numbers. Total revenue was up 3% to $3.8 billion, organic revenue was flat, adjusted gross margin held at 30.2%, and adjusted EPS landed at $0.80. Those are the financials. The channel signals are where the article gets interesting. Pro conversions are doing the work in Tools & Outdoor, but the product category mix matters. Engineered Fastening growth is uneven across end markets. DEWALT brand investment is intensifying in ways that affect the counter. And management reaffirmed full-year guidance, which is its own signal.

Pro Conversions Held Tools and Outdoor Steady

Inside the Tools & Outdoor segment, Stanley Black & Decker reported $3.336 billion in net sales, up 2% reported with organic revenue down 1%. Pricing added 4%, currency added 3%, and volume declined 5%. Adjusted segment margin was 8.7%, down 90 basis points year-over-year, on growth investments, mix shift toward lower-margin outdoor products, and tariff costs that pricing did not fully cover.

In its own deck, the company pointed to higher rates of professional conversions in the U.S. commercial and industrial channel, combined with stronger international results in prioritized markets and an early sell-in ahead of the Spring outdoor season, as the offsets to North America retail softness.

Underneath that segment number, the product mix tells a more useful story for distributors and reps. Power Tools organic revenue was down 2%. Hand Tools, Accessories, and Storage organic revenue was down 3%. Outdoor Power Equipment was up 1% organically, led by preseason demand for spring 2026, especially ride-on and zero-turn mower offerings. Geographically, North America was down 2%, Europe was up 1%, and the rest of the world was flat.

That breakdown changes the narrative. Power tools and hand tools were soft on both consumer and pro sides, even with the pro conversion tailwind helping at the margins. The outdoor +1% was sell-in timing for the spring season, not a real demand surge. Distributors stocking spring outdoor equipment should not read +1% organic growth as a category-wide tailwind. And the brighter spot is international, where prioritized markets are outpacing the domestic picture.

For the Stanley Black Decker industrial channel, this is the key dynamic. Pro conversions are holding up the segment while consumer retail weakens, but the pro side itself is still working through soft volume. Distributors that stock and merchandise the right pro SKUs capture the conversion lift. Distributors that treat pro tools as a side category lose share quietly.

Engineered Fastening Growth Has a Soft Spot for Industrial

Engineered Fastening posted $511 million in net sales, up 10% reported and 7% organically, with 190 basis points of segment margin expansion to 12.0%. That is a strong quarter on its face. But the composition matters.

Aerospace was up 31% organically. Automotive was up 4% organically and outperformed its market, helped by North American demand and global fastener systems for auto OEMs. Those two end markets carried the segment. Industrial volume, by contrast, declined. The release described the industrial softness as a partial offset to the gains.

For distributors serving aerospace MRO, automotive OEMs, and tier-one suppliers, this is encouraging. Demand at the application level is real and the company’s fastening business is participating in it. For distributors serving general industrial accounts, the picture is less clean. Industrial fastening softness is consistent with what other industrial supply data has shown in recent quarters. End-market demand is uneven, and treating industrial as a single bucket is a poor read of what is actually happening in branch sales.

This is a quarter where line-item and end-market visibility matters more than segment headlines.

DEWALT Brand Investment Will Show Up at the Counter

The clearest signal in the deck for industrial supply was the brand activation strategy. The company called out an expanded field team and trade specialists driving meaningful traction with channel partners, more than 200 DEWALT PERFORM & PROTECT products supporting commercial and industrial demand, and an initial product refresh that is now underway.

For distributors and reps, this translates into more cooperative selling, more counter-day support, and more new SKU introduction. The PERFORM & PROTECT line is positioned around dust containment, vibration control, and safer work environments. Those features sell into commercial construction, MRO, and trade contractor accounts. They also sell on jobsite compliance, which is increasingly a procurement requirement, not a preference.

Stanley Black Decker industrial channel partners should expect more aggressive channel programs through the rest of 2026. The company stated it is on-pace to return Tools & Outdoor to growth by mid-year. That is a statement of intent backed by visible field investment. The distributors and reps that lean into the cooperative motion will get the benefit.

Pricing Held, and More Tariff Pass-Through Is Coming

Pricing contributed 4% to Tools & Outdoor and 1% to Engineered Fastening in Q1. Adjusted gross margin held at 30.2%, down only 20 basis points year-over-year, despite tariff and inflation pressure. That price discipline is now familiar. What is new is the tariff overlay.

The deck states that, in line with a February 20 Supreme Court decision, the current scenario assumes Section 232 tariffs apply for 150 days through late July, with Section 301 tariffs reverting to IEEPA-equivalent levels after that window. Tariff refunds are a possibility, though Stanley Black & Decker’s guidance excludes them. Management said the recent Section 232 changes should not materially affect 2026 guidance.

The practical message is straightforward. The company is continuing to take pricing to offset tariff costs, and distributors should expect more communications about list price moves, surcharges, and program pricing through the summer. Independent distributors that have not built tariff communication routines for end users are going to get caught between OEM price increases and customer pushback. This is a process problem, not a market problem, and the distributors that solve it will protect margin.

CAM Divestiture Closes the Deleveraging Chapter

Stanley Black & Decker completed the sale of Consolidated Aerospace Manufacturing on April 6 for approximately $1.6 billion in net proceeds. The vast majority of those proceeds were used to reduce debt in the second quarter. Net debt to adjusted EBITDA dropped from 5.9x at the end of 2023 to a forecast of approximately 2.5x by the end of 2026.

For the channel, this is a structural detail with practical implications. A more focused company, with a healthier balance sheet and less distraction from non-core businesses, is a more consistent channel partner. It also means more capital available for brand activation, product development, and field investment, all of which flow through to the distributors and reps that carry the line.

The longer-term target is an adjusted gross margin of 35% to 37%, up from 30.2% in Q1. That trajectory will not be linear, but it sets the direction for how Stanley Black & Decker will think about pricing, mix, and channel investment over the next several years.

The Stanley Black Decker Industrial Channel Read

Pulling it together, the Stanley Black Decker industrial channel takeaways from Q1 2026 are more useful than the headline.

Pro conversions in the commercial and industrial channel are the dynamic worth tracking, but power tools and hand tools were still soft and the outdoor +1% was sell-in timing rather than a real demand surge. Engineered Fastening growth is concentrated in aerospace and automotive, with general industrial soft, so end-market visibility matters. DEWALT field investment is going to intensify, which creates cooperative selling opportunities for distributors and reps that lean in. Tariff-driven pricing actions will continue, and distributors need disciplined communication processes to avoid margin leakage. The CAM divestiture clears the way for a more focused Stanley Black & Decker as a channel partner.

Management reaffirmed full-year 2026 adjusted EPS guidance of $4.90 to $5.70 and said sales, margin, and cash performance remain on track. For distributors making inventory commitments and reps making territory plans, that reaffirmation is a useful signal. Management is not pulling back from its annual targets despite a flat organic Q1 and tariff uncertainty. The more useful question for the industrial channel is whether your branch teams, product mix, and rep coverage are positioned to capture the pro conversion trend and the brand investment behind it.

If this aligns with what you are seeing in your market, I would like to compare notes. CMG works with manufacturers, distributors, and rep firms who want clearer strategy, stronger channel performance, and better alignment across the field. If you are exploring ways to strengthen your commercial approach, reach out and let’s talk through what you are trying to build.

Leave a Reply