As an analyst for the past 20 years, I have relied on key economic indicators as foundational to prepare forecasts for leadership to make informed business decisions. Two of those key foundational indicators were Durable Goods Purchases and Business Capital Investment, but those indicators have had much change the past 5 years.

The once bellwether and predictable indicator of business investments, durable goods purchases and its subcomponent, business capital investment, or CAPEX, has swung wildly since early 2020. In fact, the volatility is in the 99th percentile of historical movements. A period of pronounced swings began with the onset of the pandemic, which caused severe disruptions in orders, especially for categories like commercial aircraft, and nondefense capital goods, has continued through 2025.

Why Does it Matter?

Durable goods refer to tangible products that can be stored or inventoried and that have an average life of at least three years. Durable goods are typically expensive and therefore tend to be purchased when there is confidence in the economy. New orders for durable goods are a leading indicator, meaning when purchases increase it typically hints at an improvement to the economy. On the flip side, when the new orders trend down it is indicating a lack of confidence in the economy.

Durable goods orders are correlated to the performance of industrial supply and electrical distributors, although the correlation is not perfectly linear and is influenced by sector specific dynamics. Research confirms that an increase in durable goods orders often precede upturns in business investment, causing an increase in demand for distribution of industrial products such as fasteners, electrical components, safety equipment, maintenance supplies, etc.

During periods when durable goods orders surge (e.g., May 2025 saw a 16% jump), this often translates to higher sales volumes for distributors that serve OEMs, manufacturing plants, and contractors, as these businesses need more parts and operating supplies to fulfill their own rising order books, as businesses must stock and supply more parts and tools to support elevated production levels.. A recent MDM post referenced distributors’ optimism and pricing adjustments in response to durable goods trends, further underscoring their tight linkage.

For other distributors, such as HVAC, other indicators may have a stronger correlation than durable goods, such as manufacturer revenue, construction activity and renovation cycles, seasonal trends and consumer confidence and should be monitored. And for electrical distributors, key indicators are construction activity and construction starts. Building permits are a good leading indicator, and factors that influence project financing such as inflation and interest rates, should be monitored closely.

Recent Trends

The industrial manufacturing sector is experiencing a dramatic recalibration in 2025, as the durable goods data reveals both explosive growth as well as uncertainties. A key data point illustrating this is the aerospace and capital goods industries, which present a paradoxical landscape: record-breaking aircraft orders coexist with macroeconomic headwinds that swiftly reverse gains. The May 2025 durable goods report, showed a 16.4% surge in orders, the sharpest increase since 2024, driven by a 230% spike in nondefense aircraft orders. Boeing’s May performance was noteworthy, with 303 aircraft orders compared to just 8 in April , a 1,769% increase! This was driven by the landmark deal with Qatar Airways during President Trump’s Gulf visit, but the underlying dynamics are a bit more complex. The spike appears to reflect front-running behavior as companies anticipate further tariff hikes under the current administration, rather than a fundamental shift in long-term demand.

This was followed by June’s 9.3% contraction, the largest monthly decline since 2020, as transportation equipment drove the decrease, declining 22.4% drive home this point. Shifting demand patterns and policy-driven volatility are reshaping industrial landscape, in real-time.

While the aerospace surge is dramatic and headline capturing, the broader capital goods sector tells a more nuanced story. Outside of the transportation sector, the volatility may be less extreme but it is still evident; core durable goods orders (excluding aircraft), have held up better with a 0.5% increase in June 2025. The three-month average of durable goods orders reached record highs in early 2025, showing resilience even as headline numbers fluctuated wildly, with order backlogs also at record levels. This was mainly due to deferred and pent-up demand from earlier supply disruptions and policy-driven spikes, heightened by aggressive tariff policies in 2025, which led to “front-loading”, followed by order declines as inventories adjusted.

These figures indicate that while the aerospace sector is experiencing a brief but intense upsurge, the rest of the capital goods market is still navigating a fragile recovery.

Business investment and CAPEX trends display a similar volatility, mirroring macroeconomic policy uncertainty and the impact of tariffs. Volatility for CAPEX remains above historical averages. After robust investment in equipment and factory building in 2023–2024, momentum plateaued by late 2024, with companies accelerating CAPEX at the start of 2025 but then sharply pulling back following new U.S. tariff announcements and the resulting uncertainty and with it, lower business confidence.

The key nondefense capital goods orders (a proxy for business investment) spiked by over 50% in May 2025 but plunged 24% in June, illustrating sensitivity to policy news and trade conditions. This “boom-bust” pattern is closely linked to businesses anticipating and then reacting to policy changes. On top of the uncertainty, certain government stimulus and infrastructure initiatives expired.

Monthly tracking from VettaFi Advisor Perspectives shows the core CAPEX y-o-y percent changes for durable goods and core CAPEX since the turn of the century.

The pattern of volatility has been especially acute in sectors like transportation, manufacturing, and technology. For example, AI and cloud investments remain robust, outpacing historical averages, while capital outlays in core industrial sectors fluctuate more sharply in response to policy and demand swings. The electrical manufacturing and distribution sectors remain some of the most exposed industries to these policy and demand swings.

The front-loading of orders to avoid anticipated tariff increases means that a portion of this demand may not be repeatable. Moreover, the broader economic environment – with the Fed monitoring inflationary pressures from trade policies and global machine tool markets declining 3-4% in 2025 – suggests that the industrial sector’s recovery may be short-lived and the sustainability of these gains remains questionable.

Businesses must now operate with an unusually high degree of caution, carefully monitoring policy details and timing purchases and investments amid shifting macroeconomic signals.

The volatility in these data points reflects a deeper structural challenge: the industry’s exposure to policy-driven uncertainty. President Trump’s trade policies have created a highly unpredictable environment, with tariffs on copper, steel, aluminum, and other critical inputs creating a cost shock for manufacturers, with electronics among the most exposed. See Cognitive Market Research’s blog from April and an article in Industry Select comparing the most tariff impacted industries.

The capital goods sector faces additional headwinds from global competition. Western manufacturers are struggling to maintain market share against Chinese competitors, particularly in electronics, lighting and EV technologies. This competitive pressure is exacerbated by the lack of localized development in the U.S. market, exposing domestic producers to supply chain vulnerabilities. There has been positive news of nearshoring of manufacturing and increased investments, but these will take time.

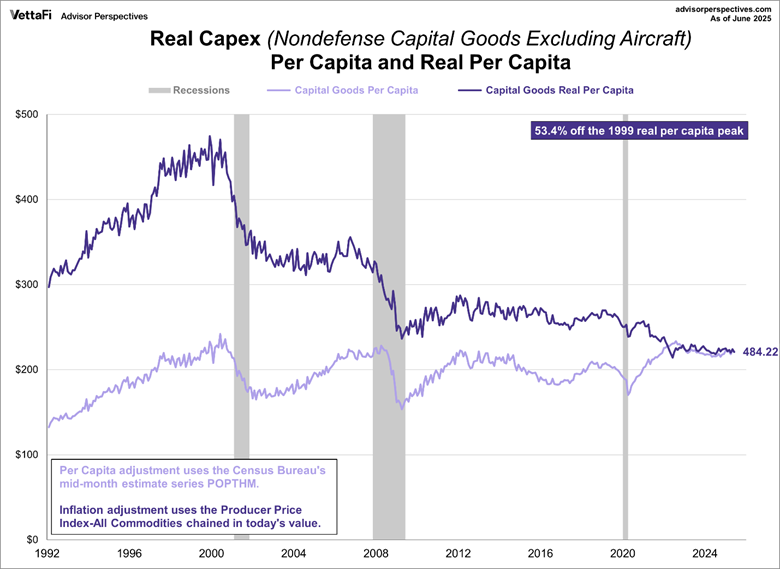

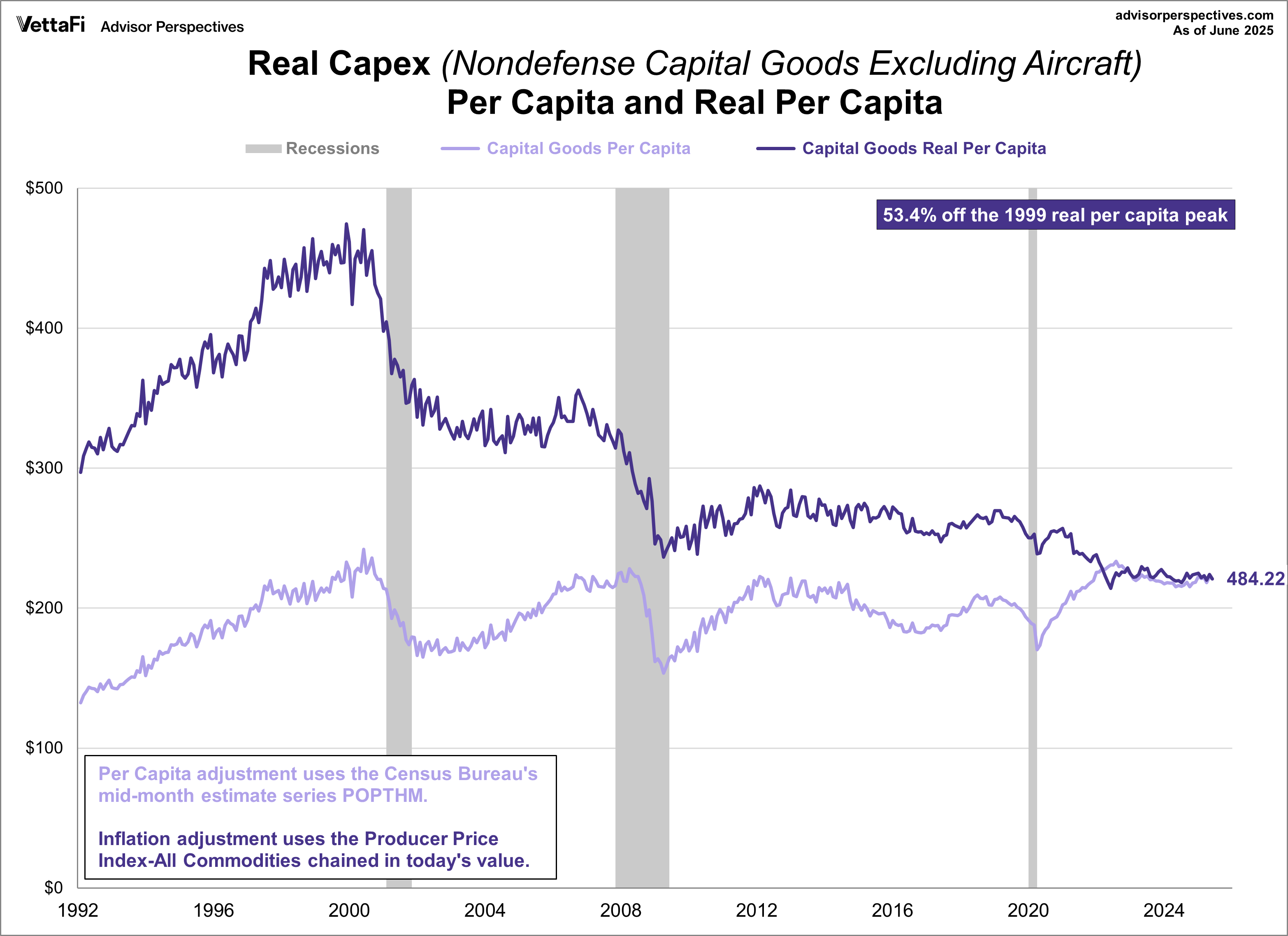

Another perspective is to adjust core CAPEX for both inflation and population growth. This gives the “real” durable goods orders per capita and could be considered a more accurate view to evaluate trends. What it shows is a generally downward slope, which could be attributable to greater productivity or less investment overall, as household income has eroded. But that is a question for further analysis.

{kind=link}

Nonetheless, looking ahead, the industrial manufacturing sector will likely remain in a state of flux. The durability of the current rebound will depend on the resolution of trade policy uncertainties and the pace of economic recovery. Monitor several key indicators: the trajectory of core capital goods orders, the impact of tariffs on production costs, the evolution of global supply chain strategies, and The Federal Reserve’s response to inflationary pressures from trade policies.

As always, we appreciate your support and comments, so please feel free to reach out to me with any questions.

Leave a Reply